Source: Pixabay.com

Despite increasing drag of trade tariffs and swirling cross-currents of currency valuations curtailing global growth causing overseas markets in bear territory, the U.S. stock market keeps powering higher.

And judging from the Volatility Index, or VIX traders expect the calm to continue even as we head into the notoriously turbulent month of October.

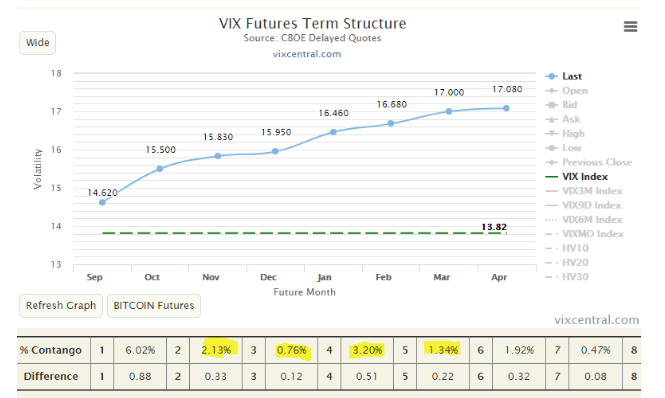

The term structure of the VIX futures — the difference in prices for various timeframes — has flattened considerably over the past few months. Historically, under normal cantango, the spread is 5%-7% from one month to next.

As you can see, once you move beyond the 1st to 2nd-month spread, it is a minuscule 1%-2%.

Source VIXCentral.com

A few of reasons for this flattening are; after February’s debacle, one various VIX related exchange traded funds blew up. People are once again getting comfortable selling option premium.

Also, much of what drives the term structure is the skew, or difference in implied volatility across various strike prices. And right now, nobody is paying a premium for far out-of-the-money puts. Meaning, people don’t foresee a major market correction or the need for portfolio protection.

Whether this turns out to be misplaced complacency or a reliable prediction remains to be seen.